The 3-6-9 rule in finance is not one single official law, but a practical guideline used in different areas of money management—especially in budgeting, saving, investing, and financial planning. Depending on the context, it usually refers to proportional targets that help people manage risk, time, and money more wisely.

At its core, the 3-6-9 rule is about balance and structure:

- 3 = short-term focus

- 6 = medium-term stability

- •9 = long-term growth

Let’s explore how this rule is used in different parts of finance.

1. The 3-6-9 Rule in Personal Budgeting

In personal finance, the 3-6-9 rule is often used to divide your money goals by time.

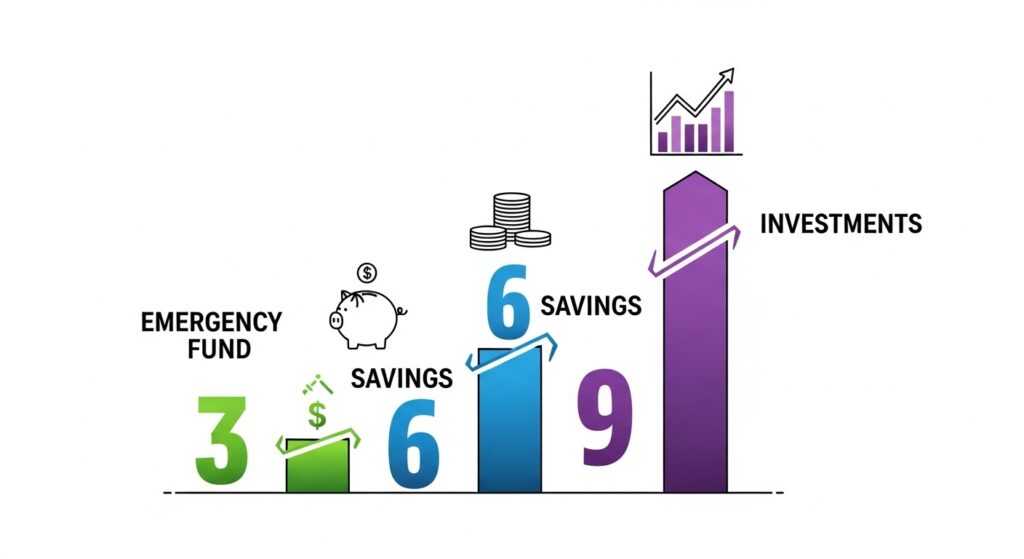

???? 3 Months – Emergency Readiness

You should aim to save at least 3 months of essential expenses.

This money is for:

• Job loss

• Medical emergencies

• Unexpected bills

Example:

If your monthly expenses = $1,000 Your 3-month emergency fund = $3,000

???? 6 Months – Financial Stability

After reaching 3 months, you build toward 6 months of expenses saved.

This gives you:

• Peace of mind

• Protection from long-term income loss

• Strong financial stability

Example:

- Monthly expenses = $1,000

- 6-month fund = $6,000

- ???? 9 Months – Financial Freedom Zone

Reaching 9 months of savings means you are financially flexible.

You can:

• Change jobs

• Start a business

• Handle big life changes

At this stage, your money works as a safety net and opportunity fund.

2. The 3-6-9 Rule in Investing

In investing, the 3-6-9 idea is used to structure time horizons and risk management.

???? 3 Years – Short-Term Investments

For goals within 3 years:

• Use low-risk investments

• Focus on capital protection

Examples:

• Savings accounts

• Fixed deposits • Money market funds

???? 6 Years – Balanced Growth

For 3–6 year goals:

• Mix safety + growth

• Use diversified investments

Examples:

• Mutual funds

• Balanced portfolios

• Index funds

???? 9+ Years – Long-Term Wealth

For 9 years or more:

• You can take more risk

• Focus on growth assets

Examples:

• Stocks

• Equity mutual funds

• Retirement funds

This part of the rule helps investors match time with risk.

3. The 3-6-9 Rule in Income Allocation

Some financial planners use the 3-6-9 rule to divide income into three main parts:

- Rule Part

- Purpose

- %

- 3

- Living Expenses

- 30%

- 6

- Savings & Investing

- 60%

- 9

- Lifestyle & Goals

- 10%

Another version is:

• 30% Needs

• 60% Financial Growth

• 10% Enjoyment

This version encourages people to:

- Live responsibly

- Save aggressively

- Enjoy life wisely

4. The 3-6-9 Rule in Debt Management

Debt planning also uses the 3-6-9 structure:

???? 3 Types of Debt You Should Avoid

• Credit card debt

• Payday loans

• High-interest consumer loans

???? 6 Rules for Smart Borrowing

- Borrow only for assets

- Compare interest rates

- Check repayment ability

- Avoid emotional buying

- Maintain good credit

- Always read terms

???? 9 Steps to Get Out of Debt

List all debts

- Stop new borrowing

- Create a budget

- Build emergency fund

- Pay smallest debts first

- Increase income

- Cut expenses

- Negotiate with lenders

- Track progress

5. The 3-6-9 Rule in Business Finance

In business, the 3-6-9 rule helps in planning cash flow and growth.

???? 3 Key Financial Statements

• Income Statement

• Balance Sheet

• Cash Flow Statement

???? 6-Month Cash Reserve

Businesses should keep at least 6 months of operating expenses saved to survive slow periods.

???? 9-Month Growth Plan

Every business should prepare a 9-month expansion or strategy plan that includes: • Revenue targets • Marketing budgets • Investment needs • Hiring plans

6. The 3-6-9 Rule in Goal Setting

The rule also applies to financial goal planning:

- ???? 3 Short-Term Goals (0–1 year)

Examples:

• Build emergency fund

• Pay off a small loan

• Save for gadgets

???? 6 Medium-Term Goals (1–5 years)

Examples:

• Buy a car

• Start a business

• Pay off student loan

???? 9 Long-Term Goals (5–20 years)

Examples:

• Buy a house

• Children’s education

• Retirement

This keeps your money aligned with your life priorities.

7. Why the 3-6-9 Rule Works

The power of the 3-6-9 rule comes from simplicity and structure.

It helps you:

- Avoid emotional money decisions

- Plan for emergencies

- Invest with clarity

- Reduce financial stress

- Build long-term wealth

Instead of random saving and spending, you follow a system.

8. Real-Life Example

Let’s say Ali earns $1,500/month.

Using the 3-6-9 approach:

• Monthly expenses = $800

• Emergency fund target (6 months) = $4,800

• Investment target = long-term (9+ years)

• Short-term savings = $300

• Long-term investing = $400

In 2 years:

- He has emergency safety

- He invests for retirement

- He stays debt-free

9. Common Pitfalls

- It is not magic, the 3-6-9 rule

- It’s not a guarantee of profit

- It’s not a legal regulation

It’s just a system through which you structure your finances.

10. How to Implement the 3-6-9 Rule in Your Life Today

- Step 1: Work out your monthly expenditure

- Step 2: Establish your 3-month emergency target

- Step 3: Build toward 6 months

- Step 4: Begin Long-term investment > 9 years

- Step 5: Review every 6 months

Final Thoughts

Some finance thought processes are like the 3-6-9 rule, which helps you understand time, money, and stability very well.

It does so by:

• Guard thyself (3)

• Stabilize your life (end

• Grow your future (9) Be it a student, employee, freelancer, or businessman-the rule provides structure and direction to one’s finances.