What Is the 7/5/3-1 Rule in Mutual Funds?

Mutual fund investing has been considered a bit complicated by many, especially for beginners. With so many categories of funds, market risks, return expectations, and investment horizons, most investors often seek some simple rules of thumb to help them make their choice. Of late, one such highly debated rule in the Indian mutual fund space is the 7/5/3-1 rule in mutual funds.

This rule helps an investor get realistic return expectations in various mutual fund schemes, matching his or her risk profile and investment horizon. Instead of getting carried away by unrealistic return expectations or market hype, the 7/5/3-1 rule is aimed at ensuring disciplined long-term investing.

We will discuss in this article what 7/5/3-1 rule in mutual funds is, how it works, why is this important, its advantages and limitations, and how can an investor use this to construct a balanced portfolio.

Understanding the Concept Behind the 7/5/3-1

On the other hand, the 7/5/3-1 Rule can never be considered a formula for guaranteed performance because it relates to a return on investment framework. It proposes the average annual returns investors should reasonably expect from various kinds of mutual funds over a long-term investment period.

This rule has been derived based on historical facts, market behavior, and the intrinsic correlation between risk and return.

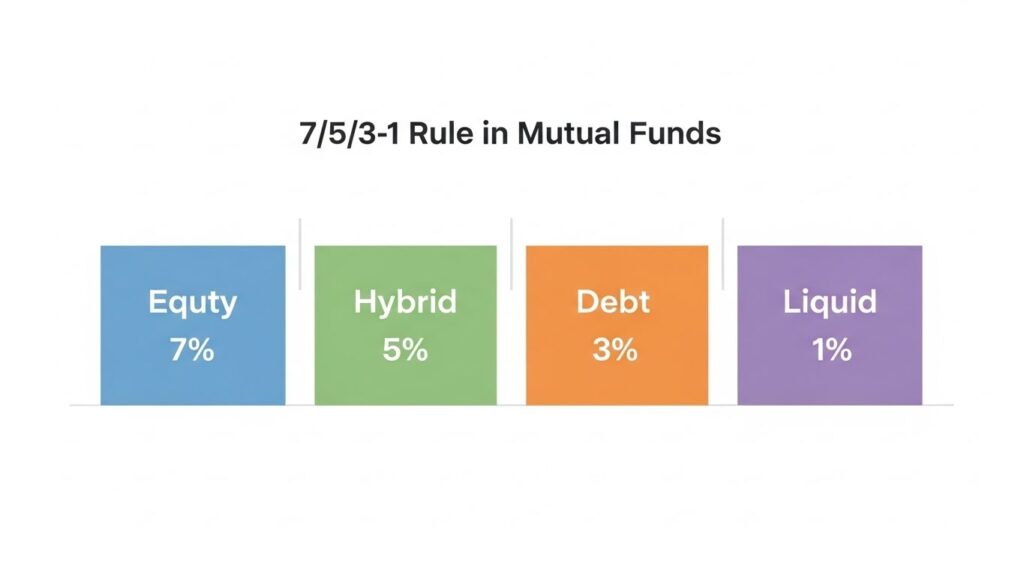

The Numbers Explained

- Equitable Funds Brand Sheldon Corporation

Annual Expected Return Expected Annual Return

- Equity Mutual Funds

Equity

~7

- Hybrid/Balanced Funds

~5

Debt Mutual Funds

~3

Liquid/Ultra-Short Term Funds

~1

These are long-term average return percentages, not short-term returns. There are no guarantees.

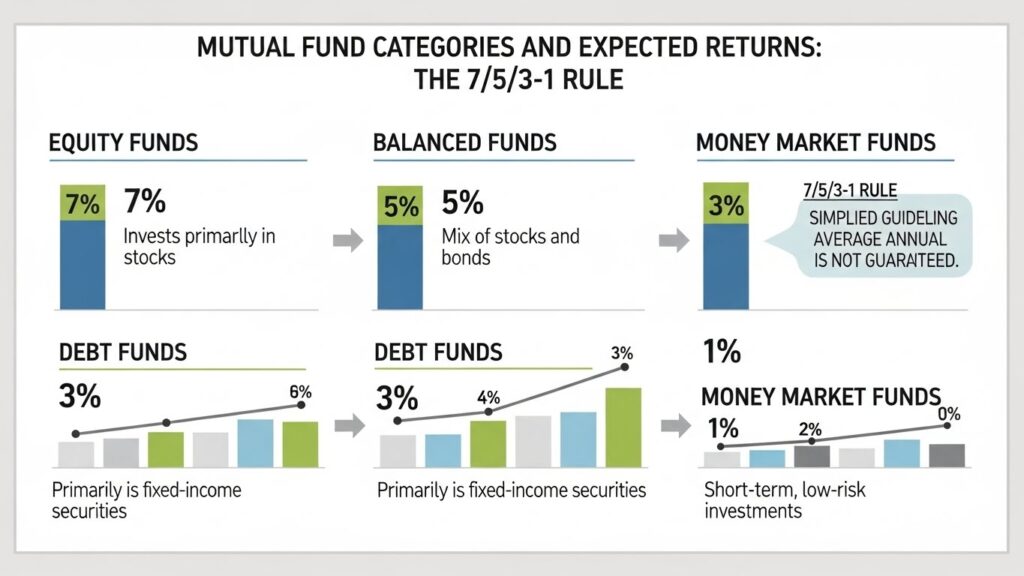

What is the 7/5/3-1 Rule for Mutual Funds?

The rule of 7/5/3-1 in mutual funds holds that

Equity Mutual Funds: Equity Mutual Funds could possibly provide an average yearly return of 7%

Hybrid/ Balanced Funds: These may yield returns around 5% annually

Debt mutual funds can fetch around 3% returns every year

Liquid or overnight funds can make about 1% return in a year

This is to encourage investors to make their expectations realistic and to avoid emotional and disappointing investment choices in the stock market.

Why is the 7/5/3-1 rule so important?

Most investors invest in mutual funds with high expectations of returns-15%, 20%, or even 25%-year in and year out. When markets correct or funds underperform, panic selling follows suit.

The 7/5/3-1 rule provides help in:

- Establishing realistic return expectations

- Understanding risk vs reward

- Choosing the right fund category

- Steer clear of short-term speculation

- Encouraging the long-term creation of wealth

- Detailed Breakdown of the 7/5/3-1 Rule

1. Equity Mutual Funds – 7% Return Expectation

Equity mutual funds invest primarily in stocks. They have the highest risk but also carry the highest growth potential over the long run.

Why 7%?

Equity markets are volatile in the short term.

Long-term equity returns tend to average out.

Inflation-adjusted or real returns are more realistic at this level.

Suitable for:

- Long-term investors (5–10+ years)

- The goals of creating wealth

- retirement planning

Investors with high risk tolerance may view the current offers as more attractive.

While this may mean 15–20% returns some years, other years it may mean negative returns. Often, over time, the average settles around 7%.

2. Hybrid/Balanced Funds – Return Expectation of 5%

Hybrid funds are invested in a mix of equity and debt, hence balancing the volatility for moderate growth.

Why 5%?

Equity portion provides growth.

Debt portion provides stability.

Lower risk as compared to pure equity funds

Suitable for:

- Moderate risk investors

- Medium-term objectives (3–5 years)

- Debt investors moving into equity

Hybrid funds are most suited for investors seeking balanced growth with lower volatility.

3. Debt Mutual Funds – 3% Return Expectation

Debt mutual funds invest into fixed income security instruments such as bonds, government securities, and money market instruments.

Why 3%?

Returns are still bound with interest rates.

Lower volatility than equity Designed to preserve capital rather than than growth

Suitable for:&#

- Conservative investors

- Capital Protection

================

Short to medium term financial objectives

Debt funds can offer marginally higher returns compared to normal savings accounts, but they are not suited for aggressive growth opportunities.

4. Liquid/ Ultra Short-Term Funds – 1% Return Expectation

Liquid funds park money in extremely short-term markets with negligible risk.

Why 1%

Liquidity and Safety Are Emphasized

Investments are like savings accounts.

Extremely Low Volatility

Applicable for:

- Parking emergency funds

- Short-term cash management

As

Corporate Treasuries

Liquid funds, while not wealth builders, are nevertheless important sources of stability and liquidity.

The Psychology Behind 7/5/3-1 Rule

One of the main advantages of mutual funds that use the rule of 7-5-3-1 is its behavioral aspect.

It assists investors:

- Don’t panic in falling markets

- The idea

- Stay the course during market fluctuations

5. Reduce greed during bull markets

Emphasize Asset Allocation over Timing

Investors make wise decisions through the management of expectations.

How to Apply the 7/5/3-1 Rule to Your Investment Portfolio Planning

Step 1: Determine Your Risk Profile

Step

Aggressive → More equity exposure * Moderate \-> Hybrid allocation Conservative → Debt-heavy portfolio

2. Match Goals with Time Horizon

Short term → Liquid or debt funds

Medium term → Hybrid funds

Long term → Equity Funds

Retailer 1 Retailer 2

To realistically forecast the future value, the 7/5/3-1 rule can

Example of Using the 7/5/3

Assume an investment of ₹5,00,000 for various purposes:

- ₹2,00,000 in equity funds → ~7

- ₹1,50,000 in hybrid funds → ~5

- ₹1,00,000 in debt funds → ~3

- ₹50,000 in liquid funds → ~1%

This provides “a diversified approach balancing growth, stability, and liquidity.”

Benefits of Using 7/5/3

Practices long-term investment

Reduces emotional investing

Facilitates realistic expectations

Aids in Goal-Oriented Planning

Limitations of the 7/5/3

Although it has its utility, it has some limitations:

- Return on investment not guaranteed

- Investment

- Market cycles may vary

- Inflation effect can differ

Individual fund performance may vary Not appropriate for Intraday Trading That is why this guideline should not be followed as a formula. Is the 7/5/3-1 Rule Still Valid in

Yes, because the 7/5/3-1 rule in mutual funds is applicable in that it aims at fundamentals, not forecasting.

Although markets undergo change, the following relationship always applies:

- High Risk High Potential Return

- Higher risk → Higher expected return

- 7/5/3-1 Rule vs Unrealistic

- Expectation Type

Conclusion

Unrealistic (15

Disappointment and panic sales

Discpline, wealth creation

Investors who rely on grounded frameworks increase their chances of remaining invested and meeting their financial objectives.

Who Should Follow the 7/5/3-1

- Beginner Investors

- Short-term planners

- Retirement investors

Conservative and Moderate Investors

Anyone looking for disciplined investing

“Final Thoughts: What is the 7/5/3-1 rule in mutual funds?”

The 7/5/3-1 rule in mutual fund investing is a simple yet informative technique that assists investors in understanding what to reasonably expect in terms of returns from the various mutual fund schemes available in the market. Though it does not assure any certain return, it does assure clarity, structure, and emotional stability, which are far more important considerations than achieving the highest possible rates of return. With careful usage, 7/5/3-1 can prove to be a great starting tool for a proper mutual fund investment.